In this section, we will build a set of accounts to track international payments. To do this, we will use the equilibrium condition for foreign exchange markets given in Equation 30.2. We will see that the balance between a country’s purchases of foreign assets and foreign purchases of the country’s assets will have important effects on net exports, and thus on aggregate demand.

We can rearrange the terms in Equation 30.2 to write the following:

EQUATION 30.3

Exports−imports = − [(rest-of-world purchases of domestic assets) − (domestic purchases of rest-ofworld assets)]

Equation 30.3 represents an extremely important relationship. Let us examine it carefully.

The left side of the equation is net exports. It is the balance between spending flowing from foreign countries into a particular country for the purchase of its goods and services and spending flowing out of the country for the purchase of goods and services produced in other countries. The current account is an accounting statement that includes all spending flows across a nation’s border except those that represent purchases of assets. The balance on current account equals spending flowing into an economy from the rest of the world on current account less spending flowing from the nation to the rest of the world on current account. Given our two simplifying assumptions—that there are no international transfer payments and that we can treat rest-of-world purchases of domestic factor services as exports and domestic purchases of rest-of-world factor services as imports—the balance on current account equals net exports. When the balance on current account is positive, spending flowing in for the purchase of goods and services exceeds spending that flows out, and the economy has a current account surplus (i.e., net exports are positive in our simplified analysis). When the balance on current account is negative, spending for goods and services that flows out of the country exceeds spending that flows in, and the economy has a current account deficit (i.e., net exports are negative in our simplified analysis).

A country’s capital account is an accounting statement of spending flows into and out of the country during a particular period for purchases of assets. The term within the parentheses on the right side of the equation gives the balance between rest-of-world purchases of domestic assets and domestic purchases of rest-of-world assets; this balance is a country’s balance on capital account. A positive balance on capital account is a capital account surplus. A capital account surplus means that buyers in the rest of the world are purchasing more of a country’s assets than buyers in the domestic economy are spending on rest-of-world assets. A negative balance on capital account is a capital account deficit. It implies that buyers in the domestic economy are purchasing a greater volume of assets in other countries than buyers in other countries are spending on the domestic economy’s assets. Remember that the balance on capital account is the term inside the parentheses on the right-hand side of Equation 30.3 and that there is a minus sign outside the parentheses.

Equation 30.3 tells us that a country’s balance on current account equals the negative of its balance on capital account. Suppose, for example, that buyers in the rest of the world are spending $100 billion per year acquiring assets in a country, while that country’s buyers are spending $70 billion per year to acquire assets in the rest of the world. The country thus has a capital account surplus of $30 billion per year. Equation 30.3 tells us the country must have a current account deficit of $30 billion per year.

Alternatively, suppose buyers from the rest of the world acquire $25 billion of a country’s assets per year and that buyers in that country buy $40 billion per year in assets in other countries. The economy has a capital account deficit of $15 billion; its capital account balance equals −$15 billion. Equation 30.3 tells us it thus has a current account surplus of $15 billion. In general, we may write the following:

EQUATION 30.4

Current account balance = − (capital account balance)

Assuming the market for a nation’s currency is in equilibrium, a capital account surplus necessarily means a current account deficit. A capital account deficit necessarily means a current account surplus. Similarly, a current account surplus implies a capital account deficit; a current account deficit implies a capital account surplus. Whenever the market for a country’s currency is in equilibrium, and it virtually always is in the absence of exchange rate controls, Equation 30.3 is an identity—it must be true. Thus, any surplus or deficit in the current account means the capital account has an offsetting deficit or surplus.

The accounting relationships underlying international finance hold as long as a country’s currency market is in equilibrium. But what are the economic forces at work that cause these equalities to hold?

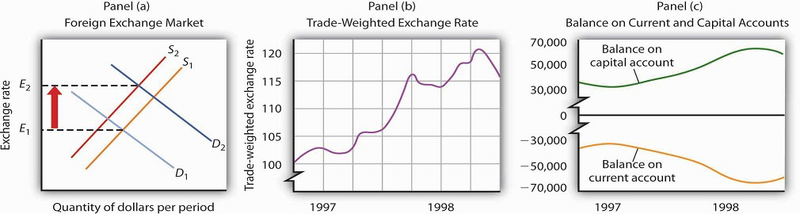

Consider how global turmoil in 1997 and 1998, discussed in the chapter opening, affected the United States. Holders of assets, including foreign currencies, in the rest of the world were understandably concerned that the values of those assets might fall. To avoid a plunge in the values of their own holdings, many of them purchased U.S. assets, including U.S. dollars. Those purchases of U.S. assets increased the U.S. surplus on capital account. To buy those assets, foreign purchasers had to purchase dollars. Also, U.S. citizens became lss willing to hold foreign assets, and their preference for holding assets increased. United States citizens were thus less willing to supply dollars to the foreign exchange market. The increased demand for dollars and the decreased supply of dollars sent the U.S. exchange rate higher, as shown in Panel (a) of Figure 30.4. Panel (b) shows the actual movement of the exchange rate in 1997 and 1998. Notice the sharp increases in the exchange rate throughout most of the period. A higher exchange rate in the United States reduces U.S. exports and increases U.S. imports, increasing the current account deficit. Panel (c) shows the movement of the current and capital accounts in the United States in 1997 and 1998. Notice that as the capital account surplus increased, the current account deficit rose. A reduction in the U.S. exchange rate at the end of 1998 coincided with a movement of these balances in the opposite direction.

Turmoil in currency markets all over the world in 1997 and 1998 increased the demand for dollars and decreased the supply of dollars in the foreign exchange market, which caused an increase in the U.S. exchange rate, as shown in Panel (a). Panel (b) shows actual values of the U.S. exchange rate during that period; Panel (c) shows U.S. balances on current and on capital accounts. Notice that the balance on capital account generally rose while the balance on current account generally fell.

- 979 reads