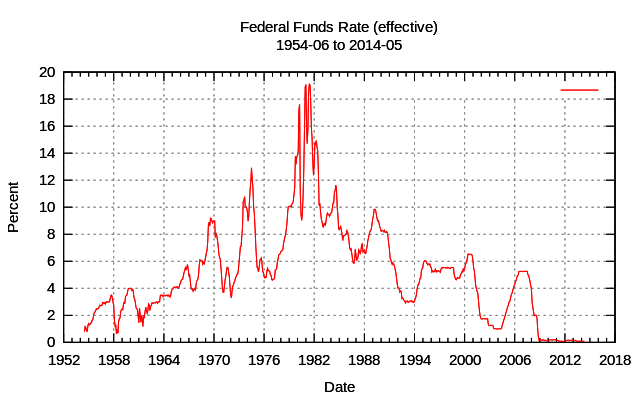

The Federal Reserve System implements monetary policy largely by targeting the federal funds rate. This is the rate that banks charge each other for overnight loans of federal funds, which are the reserves held by banks at the Fed. This rate is actually determined by the market and is not explicitly mandated by the Fed. The Fed therefore tries to align the effective federal funds rate with the targeted rate by adding or subtracting from the money supply through open market operations. The Federal Reserve System usually adjusts the federal funds rate target by 0.25% or 0.50% at a time.

Open market operations allow the Federal Reserve to increase or decrease the amount of money in the banking system as necessary to balance the Federal Reserve's dual mandates. Open market operations are done through the sale and purchase of United States Treasury security, sometimes called "Treasury bills" or more informally "T-bills" or "Treasuries". The Federal Reserve buys Treasury bills from its primary dealers. The purchase of these securities affects the federal funds rate, because primary dealers have accounts at depository institutions 1.

The Federal Reserve education website describes open market operations as follows 2:

Open market operations involve the buying and selling of U.S. government securities (federal agency and mortgage-backed). The term 'open market' means that the Fed doesn't decide on its own which securities dealers it will do business with on a particular day. Rather, the choice emerges from an 'open market' in which the various securities dealers that the Fed does business with—the primary dealers—compete on the basis of price. Open market operations are flexible and thus, the most frequently used tool of monetary policy.

Open market operations are the primary tool used to regulate the supply of bank reserves. This tool consists of Federal Reserve purchases and sales of financial instruments, usually securities issued by the U.S. Treasury, Federal agencies and government-sponsored enterprises. Open market operations are carried out by the Domestic Trading Desk of the Federal Reserve Bank of New York under direction from the FOMC. The transactions are undertaken with primary dealers.

The Fed's goal in trading the securities is to affect the federal funds rate, the rate at which banks borrow reserves from each other. When the Fed wants to increase reserves, it buys securities and pays for them by making a deposit to the account maintained at the Fed by the primary dealer's bank. When the Fed wants to reduce reserves, it sells securities and collects from those accounts. Most days, the Fed does not want to increase or decrease reserves permanently so it usually engages in transactions reversed within a day or two. That means that a reserve injection today could be withdrawn tomorrow morning, only to be renewed at some level several hours later. These short-term transactions are called repurchase agreements (repos) – the dealer sells the Fed a security and agrees to buy it back at a later date.

- 瀏覽次數:2419