The global economy is the sum total of all the national economies. Just as national economies must be in some kind of equilibrium, so the global economy's product must equal the global economy's income. In other words, what is true for the national economy must be true for the global economy:

Global product and global income must be equal.

The global economy operates much like a national economy. Thus, the circular flow diagram shown in Figure 6.1 can also be used to represent the global economy. The main difference is, of course, the tremendous diversity among the three main actors in the global economy—namely, the consumers, the producers (the firms), and the governments. Although the functions performed by these main actors are the same on the global scale as they are on a national scale, their degree of participation in both the production and the consumption of their products varies.

Statistics used to provide a quantitative measure of the global economy and to explain some of its qualitative dimensions are not very reliable. Because the intention here is to promote an understanding of the magnitude of the phenomenon rather than to settle any conceptual or empirical questions or disputes, the reader should understand that the data to follow are not definitive but merely illustrative.

Researchers and practitioners who are concerned with gaining an accurate understanding of the world economy use three main concepts to do so: population, income, and resources. The logic behind this emphasis is that people are both the producers and the consumers of resources. Thus, when population increases so does the opportunity for greater production and consumption of resources.

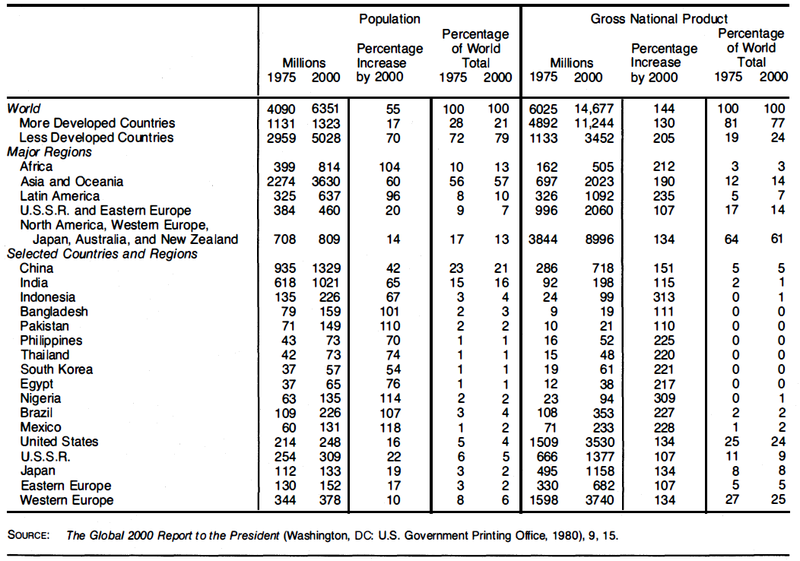

Figure 6.4 summarizes data on the earth's people and their incomes for 1975 and gives projections for the year 2000. Between 1975 and 2000 the world's population is expected to increase 55%, from 4090 million to 6351 million; the world's GNP is expected to more than double, from $6025 to $14,677 billion in constant 1975 dollars. The areas of the world that are expected to show the greatest increases in per capita income are expected to have the smallest population increases. A line drawn approximately at the level of the equator would divide the world into two very different halves: the upper half rich in money and poor in people, and the lower half poor in money and rich in people.

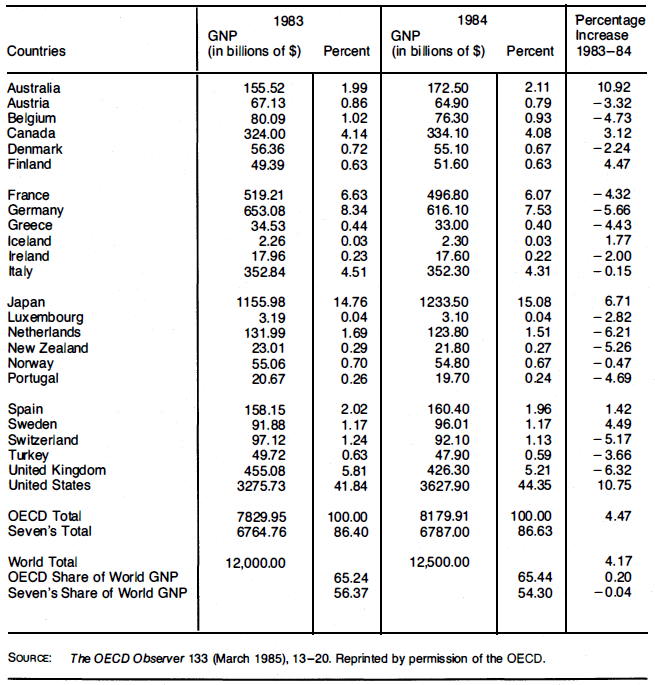

The dynamic agent within the rich industrialized world is the OECD. As noted in THE ENVIRONMENT, the twenty-four countries of the OECD are a vital part of the world economy. Figure 6.5 reveals that the OECD countries, which make up less than 15% of the world population, account for some 65% of the gross world product. Within the OECD a small number of countries, called the Group of 7 or G7, (the United States, West Germany, France, Britain, Italy, the Netherlands, and Japan) account for some 86% of the OECD's product and 56% of the world's product.

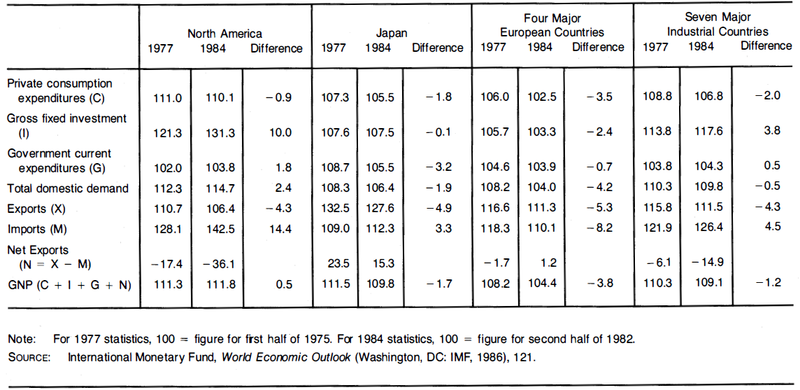

Figure 6.6 shows the changes in the basic components of aggregate demand for the industrialized countries between 1977 and 1984. Western Europe experienced the greatest decline in private consumption (-3.5 points), and the United States the least decline (-0.9 of a point). Overall, Europeans experienced the greatest decline in all major components of the GNP, and as a result their GNP declined by the largest amount (-3.8 points). The United States is the "engine of growth" or the "locomotive" for the rest of the world, as indicated by the fact that the United States' imports jumped some 14.4 points during the years shown.

The statistics in Figure 6.6 indicate that all the main components of demand (private consumption, investment, government expenditures, and net exports) have increased over the last few decades. In addition, the other component of the economy—population—has shown encouraging signs of a slowdown in growth.

In general, the global economy is essentially run by about ten industrialized countries, which combined account for over 60% of the world's output but no more than 15% of the world's population. When these countries prosper economically, almost everybody else prospers. Most of the world depends on the financing and the demand generated by these industrialized countries.

- 2566 reads