Available under Creative Commons-ShareAlike 4.0 International License.

All accounting transactions are first recorded in a journal. The most common of these is the General Journal, sometimes also known as the Book of Original Entry, because it is the first place a transaction is entered into the books. Journal Entries are made from source documents, which can be anything from receipts to invoices to bank statements.

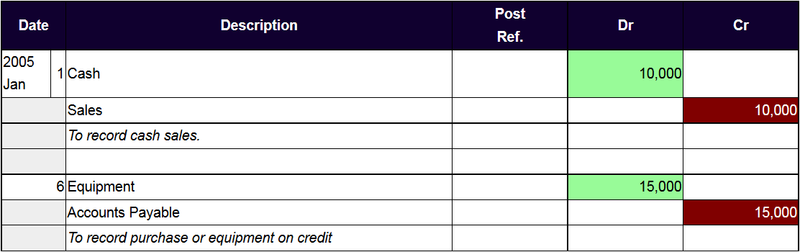

Figure 2.2 General Journal - Page 1

These two entries show the premise of double-entry accounting. Note that the form of what is written is as important as the actual text:

- Debits are always recorded first, followed by the credits.

- In keeping with the rule of "Debit = Left, Credit = Right", all accounts that are credited have their titles indented ("Sales" and "Accounts Payable" in this example).

- The year and month are only recorded once in the date column. They are recorded again at the top of every new page, and whenever the month or year changes. However, a new page is usually started at the beginning of each month, because end-of-period entries are normally recorded on a separate page.

- A description of each entry is placed on the line below the entry. While this is not required, it is good practice because, at times, account titles may not be enough to describe what actually occurred for a specific transaction.

- A blank line is inserted between entries.

The process of recording entries to a journal is called journalizing.

- 3070 reads