One hypothesis suggests that monetary policy may affect the price level but not real GDP. The rational expectations hypothesis states that people use all available information to make forecasts about future economic activity and the price level, and they adjust their behavior to these forecasts.

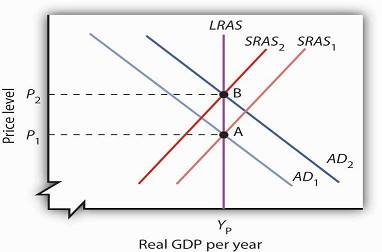

Figure 26.4 uses the model of aggregate demand and aggregate supply to show the implications of the rational expectations argument for monetary policy. Suppose the economy is operating at YP, as illustrated by point A. An increase in the money supply boosts aggregate demand to AD2. In the analysis we have explored thus far, the shift in aggregate demand would move the economy to a higher level of real GDP and create an inflationary gap. That, in turn, would put upward pressure on wages and other prices, shifting the short-run aggregate supply curve to SRAS2 and moving the economy to point B, closing the inflationary gap in the long run. The rational expectations hypothesis, however, suggests a quite different interpretation.

Suppose the economy is operating at point A and that individuals have rational expectations. They calculate that an expansionary monetary policy undertaken at price level P1 will raise prices to P2. They adjust their expectations—and wage demands—accordingly, quickly shifting the short-run aggregate supply curve to SRAS2. The result is a movement along the long-run aggregate supply curve LRAS to point B, with no change in real GDP.

Suppose people observe the initial monetary policy change undertaken when the economy is at point A and calculate that the increase in the money supply will ultimately drive the price level up to point B. Anticipating this change in prices, people adjust their behavior. For example, if the increase in the price level from P1 to P2 is a 10% change, workers will anticipate that the prices they pay will rise 10%, and they will demand 10% higher wages. Their employers, anticipating that the prices they will receive will also rise, will agree to pay those higher wages. As nominal wages increase, the short-run aggregate supply curve immediately shifts to SRAS2. The result is an upward movement along the long-run aggregate supply curve, LRAS. There is no change in real GDP. The monetary policy has no effect, other than its impact on the price level. This rational expectations argument relies on wages and prices being sufficiently flexible— not sticky, as described in an earlier chapter—so that the change in expectations will allow the short-run aggregate supply curve to shift quickly to SRAS2.

One important implication of the rational expectations argument is that a contractionary monetary policy could be painless. Suppose the economy is at point B in Figure 26.4, and the Fed reduces the money supply in order to shift the aggregate demand curve back to AD1. In the model of aggregate demand and aggregate supply, the result would be a recession. But in a rational expectations world, people’s expectations change, the short-run aggregate supply immediately shifts to the right, and the economy moves painlessly down its long-run aggregate supply curve LRAS to point A. Those who support the rational expectations hypothesis, however, also tend to argue that monetary policy should not be used as a tool of stabilization policy

For some, the events of the early 1980s weakened support for the rational expectations hypothesis; for others, those same events strengthened support for this hypothesis.

As we saw in the introduction to an earlier chapter, in 1979 President Jimmy Carter appointed Paul Volcker as Chairman of the Federal Reserve and pledged his full support for whatever the Fed might do to contain inflation. Mr. Volcker made it clear that the Fed was going to slow money growth and boost interest rates. He acknowledged that this policy would have costs but said that the Fed would stick to it as long as necessary to control inflation. Here was a monetary policy that was clearly announced and carried out as advertised. But the policy brought on the most severe recession since the Great Depression—a result that seems inconsistent with the rational expectations argument that changing expectations would prevent such a policy from having a substantial effect on real GDP.

Others, however, argue that people were aware of the Fed’s pronouncements but were skeptical about whether the anti-inflation effort would persist, since the Fed had not vigorously fought inflation in the late 1960s and the 1970s. Against this history, people adjusted their estimates of inflation downward slowly. In essence, the recession occurred because people were surprised that the Fed was serious about fighting inflation.

Regardless of where one stands on this debate, one message does seem clear: once the Fed has proved it is serious about maintaining price stability, doing so in the future gets easier. To put this in concrete terms, Volcker’s fight made Greenspan’s work easier, and Greenspan’s legacy of low inflation should make Bernanke’s easier.

KEY TAKEAWAYS

- Macroeconomic policy makers must contend with recognition, implementation, and impact lags.

- Potential targets for macroeconomic policy include interest rates, money growth rates, and the price level or expected rates of change in the price level.

- Even if a central bank is structured to be independent of political pressure, its officers are likely to be affected by such pressure.

- To counteract liquidity traps, central banks have used quantitative-easing and credit-easing strategies.

- No central bank can know in advance how its policies will affect the economy; the rational expectations hypothesis predicts that central bank actions will affect the money supply and the price level but not the real level of economic activity.

TRY IT!

The scenarios below describe the U.S. recession and recovery in the early 1990s. Identify the lag that may have contributed to the difficulty in using monetary policy as a tool of economic stabilization.

- The U.S. economy entered into a recession in July 1990. The Fed countered with expansionary monetary policy in October 1990, ultimately lowering the federal funds rate from 8% to 3% in 1992.

- Investment began to increase, although slowly, in early 1992, and surged in 1993.

Case in Point: Targeting Monetary Policy

Ben Bernanke, the chairman of the Federal Reserve Board, is among a growing group of economists who (at least under normal macroeconomic circumstances!) advocate targeting as an approach to

monetary policy. The idea, first proposed in 1993 by Stanford University economist John Taylor, calls for the central bank to set an inflation target and, if the actual rate is above or below

it, raise or lower the federal funds rate.

The approach would be a change from the policy carried out under Alan Greenspan, who chaired the board from 1987 to 2006. Mr. Greenspan, who opposed targeting, favors a discretionary

approach, one that some critics (and admirers) have called a “seat-of-the-pants” approach to monetary policy.

Targeting would not, according to Mr. Bernanke, be entirely formulaic, replacing the judgment of the Open Market Committee with a rigid rule. Mr. Bernanke has noted, for example, that if the

inflation were to increase as a result of a supply side shock (such as an increase in oil prices), then an automatic increase in the federal funds rate would not be appropriate.

One danger of using the current inflation rate as a target is that it might be destabilizing. After all, the current rate is actually the rate for the past month or past several months.

Adjusting the federal funds rate to past inflation could, given the inherent recognition and impact lags of monetary policy, easily lead to a worsening of the business cycle. Imagine that

past inflation has increased as a result of a much earlier increase in the money supply. That inflation might already be correcting itself by the time a tightening effort takes hold in the

economy. It thus could cause a contraction.

Bernanke has said that his preferred target is the expected rate of increase for the next year in the price index for consumer goods and services, excluding food and energy prices. That would

avoid the danger of relying on previous inflation rates. He has said that his “comfort zone” for expected inflation is between 1% and 2%.

The central banks of Australia, Brazil, Canada, Great Britain, New Zealand, South Korea, and Sweden adoptedtargeting. Japan and the United States did not. A study by Goldman Sachs, the

investment consulting and management firm, examined the performance of countries that did and did not engage in targeting. It found that countries that used targeting had more stable interest

rates and sustained steady growth. Japan and the United States had much more volatile stock and bond markets. In short, the results of the study tended to support the practice of targeting

inflation.

Sources: Peter Coy, “What’s the Fuss over Inflation Targeting? Business Week 3958 (November 7, 2005): 34; Justin Fox, “Who Will Replace Greenspan? Who Cares?” Fortune 152, no. 9 (October 31,

2005): 114.

ANSWERS TO TRY IT! PROBLEMS

- The recognition lag: the Fed did not seem to “recognize” that the economy was in a recession until several months after the recession began.

- The impact lag: investment did not pick up quickly after interest rates were reduced. Alternatively, it could be attributed to the expansionary monetary policy’s not having its desired effect, at least initially, on investment.

- 4785 reads