In The classical marketplace – demand and supply it was demonstrated that individual demands can be aggregated into an industry demand by summing them horizontally. The industry supply is obtained in exactly the same manner—by summing the firms’ supply quantities across all firms in the industry.

To illustrate, imagine we have many firms, possibly operating at different scales of output and therefore having different short-run MC curves. The MC curves of two of these firms are

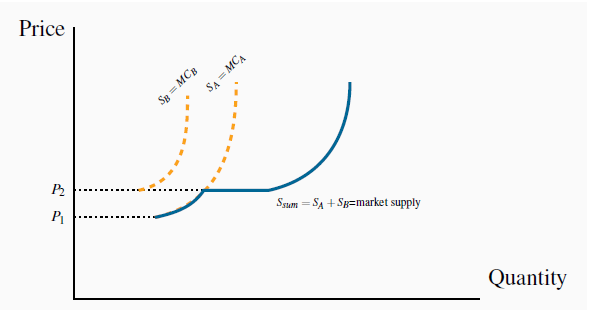

illustrated in Figure 9.3. The MC

of A is below the MC of B; therefore, B likely has a smaller scale of plant than A. Consider first the supply decisions in the price range  to

to  . At any price between these limits, only firm A will supply output – firm B does not cover its AVC in this price range. Therefore,

the joint contribution to industry supply of firms A and B is given by the MC curve of firm A. But once a price of

. At any price between these limits, only firm A will supply output – firm B does not cover its AVC in this price range. Therefore,

the joint contribution to industry supply of firms A and B is given by the MC curve of firm A. But once a price of  is attained, firm B is now willing to supply. The

is attained, firm B is now willing to supply. The  schedule is the horizontal addition of their supply quantities. Adding the supplies of every firm in the industry in this way

yields the industry supply.

schedule is the horizontal addition of their supply quantities. Adding the supplies of every firm in the industry in this way

yields the industry supply.

At any price below  production is unprofitable and supply is

therefore zero for both firms. At prices between

production is unprofitable and supply is

therefore zero for both firms. At prices between  and

and  firm A is willing to supply, but not firm B. Consequently the market supply

comes only from A. At prices above

firm A is willing to supply, but not firm B. Consequently the market supply

comes only from A. At prices above  both firms are willing to

supply. Therefore the market supply is the horizontal sum of each firm’s supply.

both firms are willing to

supply. Therefore the market supply is the horizontal sum of each firm’s supply.

Industry supply (short run) in perfect competition

is the horizontal sum of all firms’ supply curves.

Industry supply (short run) in perfect competition

is the horizontal sum of all firms’ supply curves.

Short run equilibrium in perfect competition

occurs when each firm maximizes profit by producing a quantity where P = MC.

Short run equilibrium in perfect competition

occurs when each firm maximizes profit by producing a quantity where P = MC.

- 瀏覽次數:3593