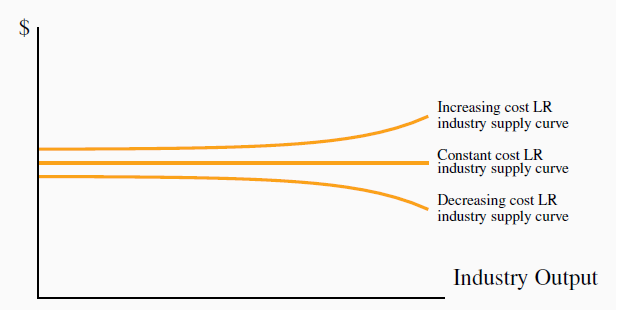

While a horizontal long-run supply is the norm for perfect competition, in some industries costs increase with the scale of industry output; in others they decrease. This may be because all of the producers use a particular input that itself becomes more or less costly with the amount supplied.

For example, when the number of fruit and vegetable stands in a market becomes very large, the owners may find that their costs are reduced because their suppliers in turn can supply the inputs at a lower cost. Conversely, it is possible that costs may increase. Consider what frequently happens in a market such as large international airports: as more flights arrive and depart delays set in – those intending to land may have to adopt a circling holding pattern while those departing encounter clearance delays. Costs increase with the scale of operation if we define the industry as the airport used by the many individual flight suppliers. In the case of declining costs, we have a decreasing cost industry; with rising costs we have an increasing cost industry. These conditions are reflected in the long-run industry supply curve by a downward-sloping segment or an upward sloping segment, as illustrated in Figure 9.9.

When individual-supplier costs rise as the output of the industry increases we have an increasing cost supply curve for the industry in the long run. Conversely when the costs of individual suppliers fall with the scale of the industry, we have a decreasing cost industry.

Increasing (decreasing) cost industry is one where

costs rise (fall) for each firm because of the scale of industry operation.

Increasing (decreasing) cost industry is one where

costs rise (fall) for each firm because of the scale of industry operation.

- 20291 reads