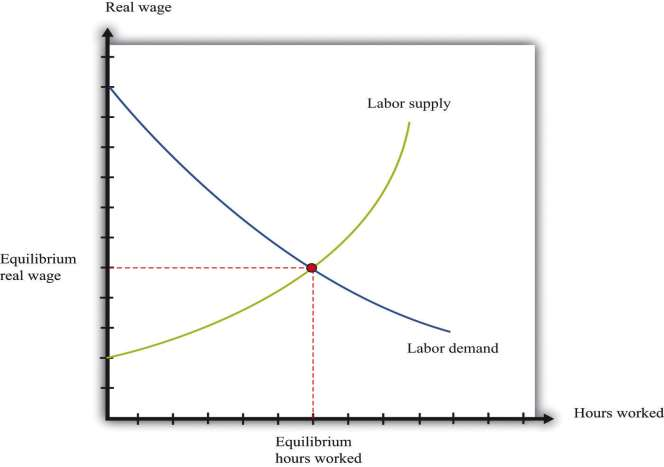

***Figure 5.4 "Equilibrium in the Labor Market" shows a diagram for the labor market. In this picture, we draw the supply of labor by households and the demand for labor by firms. The price on the vertical axis is the real wage. The real wage is just the nominal wage (the wage in dollars) divided by the price level. It tells us the amount that you can consume (measured as the number of units of real GDP that you get) if you sell one hour of your time.

Toolkit: Section 16.1 "The Labor Market" and Section 16.5 "Correcting for Inflation"

When we adjust the nominal wage in this way, we are “correcting for inflation.” The toolkit gives more information. You can also review the labor market in the toolkit.

The upward-sloping labor supply curve comes from both an increase in hours worked by each employed worker and an increase in the number of employed workers. [***We discuss labor supply in more detail in Chapter 12 "Income Taxes".***] The downward-sloping labor demand curve comes from the decision rule of firms: each firm purchases additional hours of labor up to the point where the extra output that it obtains from that labor equals the cost of that labor. The extra output that can be produced from one more hour of work is—by definition—the marginal product of labor, and the cost of labor, measured in terms of output, is the real wage. Therefore firms hire labor up to the point where the marginal product of labor equals the real wage.

The marginal product of labor also depends on the other inputs available in an economy. An economy with more physical or human capital, for example, is one in which workers will be more productive. Increases in other inputs shift the labor demand curve rightward.

The point where the labor supply and labor demand curves meet is the point of equilibrium in the labor market. At the equilibrium real wage, the number of hours that workers want to work exactly matches the number of hours that firms wish to use. ***Figure 5.4 "Equilibrium in the Labor Market" shows that equilibrium in the labor market tells us two things: the real wage in the economy and how many hours of work go into the aggregate production function.

- 2068 reads