LEARNING OBJECTIVES

After you have read this section, you should be able to answer the following questions:

What is growth accounting?

What are the different time horizons that we use in economics?

We have inventoried the factors that contribute to gross domestic product (GDP). The next step is to understand how much each factor contributes. If an economy wants to increase its GDP, is it better off trying to boost domestic savings, attract more capital from other countries, improve its infrastructure, or what? To answer such questions, we introduce a new tool that links the growth rate of output to the growth rate of the different inputs to the production function.

Toolkit: Section 16.11 "Growth Rates"

A growth rate is the percentage change in a variable from one year to the next. For example, the growth rate of real GDP is defined as

You can learn more about growth rates in the toolkit.

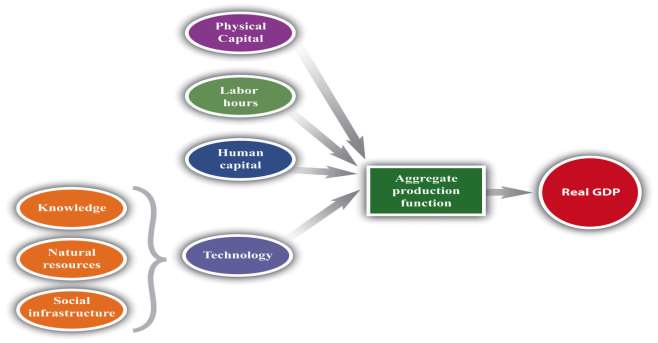

Some of the inputs to the production function—most notably knowledge, social infrastructure, and natural resources—are very difficult to measure individually. Economists typically group these inputs together into technology, as shown in ***Figure 5.10 "The Aggregate Production Function". The term is something of a misnomer because it includes not only technological factors but also social infrastructure, natural resources, and indeed anything that affects real GDP but is not captured by other inputs.

The technique for explaining output growth in terms of the growth of inputs is called growth accounting.

Toolkit: Section 16.17 "Growth Accounting"

Growth accounting tells us how changes in real GDP in an economy are due tochangesin available inputs. Under reasonably general circumstances, the change in output in an economy can be written as follows:

output growth rate = a × capital stock growth rate

***

[(1 − a) × labor hours growth rate]

***

[(1 − a) × human capital growth rate]

***

technology growth rate.

In this equation, a is just a number. Growth rates can be positive or negative, so we can use the equation to analyze decreases and increases in GDP.

We can measure the growth in output, capital stock, and labor hours using easily available economic data. The growth rate of human capital is trickier to measure, although we can use information on schooling and literacy rates to estimate this number. We also have a way of measuring a. The technical details are not important here, but a good measure of (1 − a) is simply total payments to labor in the economy (that is, the total of wages and other compensation) as a fraction of overall GDP. For most economies, a is in the range of about 1/3 to 1/2.

For the United States, the number a is about 1/3. The growth rate of output is therefore given as follows:

Because we can measure everything in this equation except growth in technology, we can use the equation to determine what the growth rate of technology must be. If we rearrange, we get the following:

To emphasize again, the powerful part of this equation is that we can use observed growth in labor, capital, human capital, and output to infer the growth rate of technology—something that is impossible to measure directly.

- 2674 reads