What factors determine the inflation rate? The price level is determined by the intersection of aggregate demand and short-run aggregate supply; anything that shifts either of these two curves changes the price level and thus affects the inflation rate. We have seen how these shifts can generate different inflation– unemployment combinations in the short run. In the long run, the rate of inflation will be determined by two factors: the rate of money growth and the rate of economic growth.

Economists generally agree that the rate of money growth is one determinant of an economy’s inflation rate in the long run. The conceptual basis for that conclusion lies in the equation of exchange: MV = PY. That is, the money supply times the velocity of money equals the price level times the value of real GDP.

Given the equation of exchange, which holds by definition, we learned in the chapter on monetary policy that the sum of the percentage rates of change in M and V will be roughly equal to the sum of the percentage rates of change in P and Y. That is,

EQUATION 31.1

%ΔM + %ΔV ≅ %ΔP + %ΔY

Suppose that velocity is stable in the long run, so that %ΔV equals zero. Then, the inflation rate (%ΔP) roughly equals the percentage rate of change in the money supply minus the percentage rate of change in real GDP:

EQUATION 31.2

%ΔP ≅ %ΔM − %ΔY

In the long run, real GDP moves to its potential level, YP. Thus, in the long run we can write Equation 31.2 as follows:

EQUATION 31.3

%ΔP ≅ %ΔM − %ΔYP

There is a limit to how fast the economy’s potential output can grow. Economists generally agree that potential output increases at only about a 2% to 3% annual rate in the United States. Given that the economy stays close to its potential, this puts a rough limit on the speed with which Y can grow. Velocity can vary, but it is not likely to change at a rapid rate over a sustained period. These two facts suggest that very rapid increases in the quantity of money, M, will inevitably produce very rapid increases in the price level, P. If the money supply grows more slowly than potential output, then the right-hand side of Equation 31.3 will be negative. The price level will fall; the economy experiences deflation.

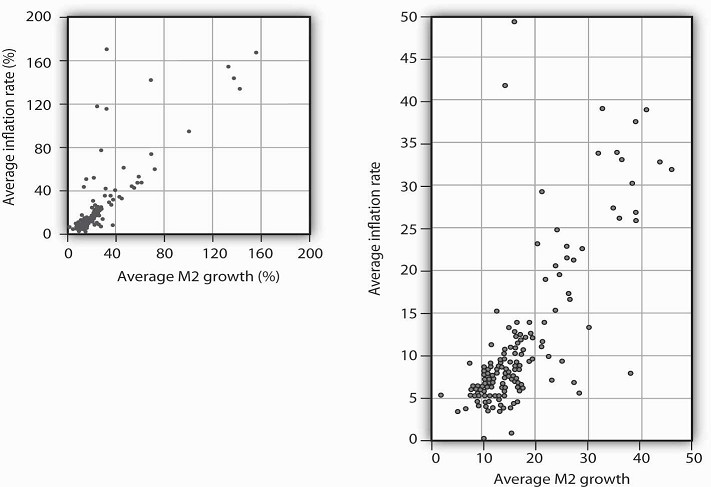

Numerous studies point to the strong relationship between money growth and inflation, especially for high-inflation countries. Figure 31.10 is from a recent study by economists Paul De Grauwe and Magdalena Polan. It is based on a sample of 160 countries over a 30-year period. Panel (a) includes all 160 countries and suggests a positive relationship between money growth and the rate of inflation. The relationship is clearly not precise, and the relationship is strengthened by the presence of countries with very high inflation rates. When the researchers break down the sample into countries with inflation rates of less than 10%, less than 20%, and less than 50%, they find that for countries with single-digit inflation the relationship between inflation and money growth is quite weak. Panel (b) shows that there is still a visible, though of course not perfect, correlation when examining countries with inflation rates of less than 50%.

Data for 160 countries over a 30-year period suggest a positive relationship between the rate of money growth and inflation. The graph shows the inflation rate against a broad definition of the money supply, M2.

Source: Paul De Grauwe and Magdalena Polan, “Is Inflation Always and Everywhere a Monetary Phenomenon?” Scandinavian Journal of Economics 107, no. 2 (2005): 245–46.

In the model of aggregate demand and aggregate supply, increases in the money supply shift the aggregate demand curve to the right and thus force the price level upward. Money growth thus produces inflation.

Of course, other factors can shift the aggregate demand curve as well. For example, expansionary fiscal policy or an increase in investment will shift aggregate demand. We have already seen that changes in the expected price level or in production costs shift the short-run aggregate supply curve. But such increases are not likely to continue year after year, as money growth can. Factors other than money growth may influence the inflation rate from one year to the next, but they are not likely to cause sustained inflation.

- 2936 reads