Available under Creative Commons-NonCommercial-ShareAlike 4.0 International License.

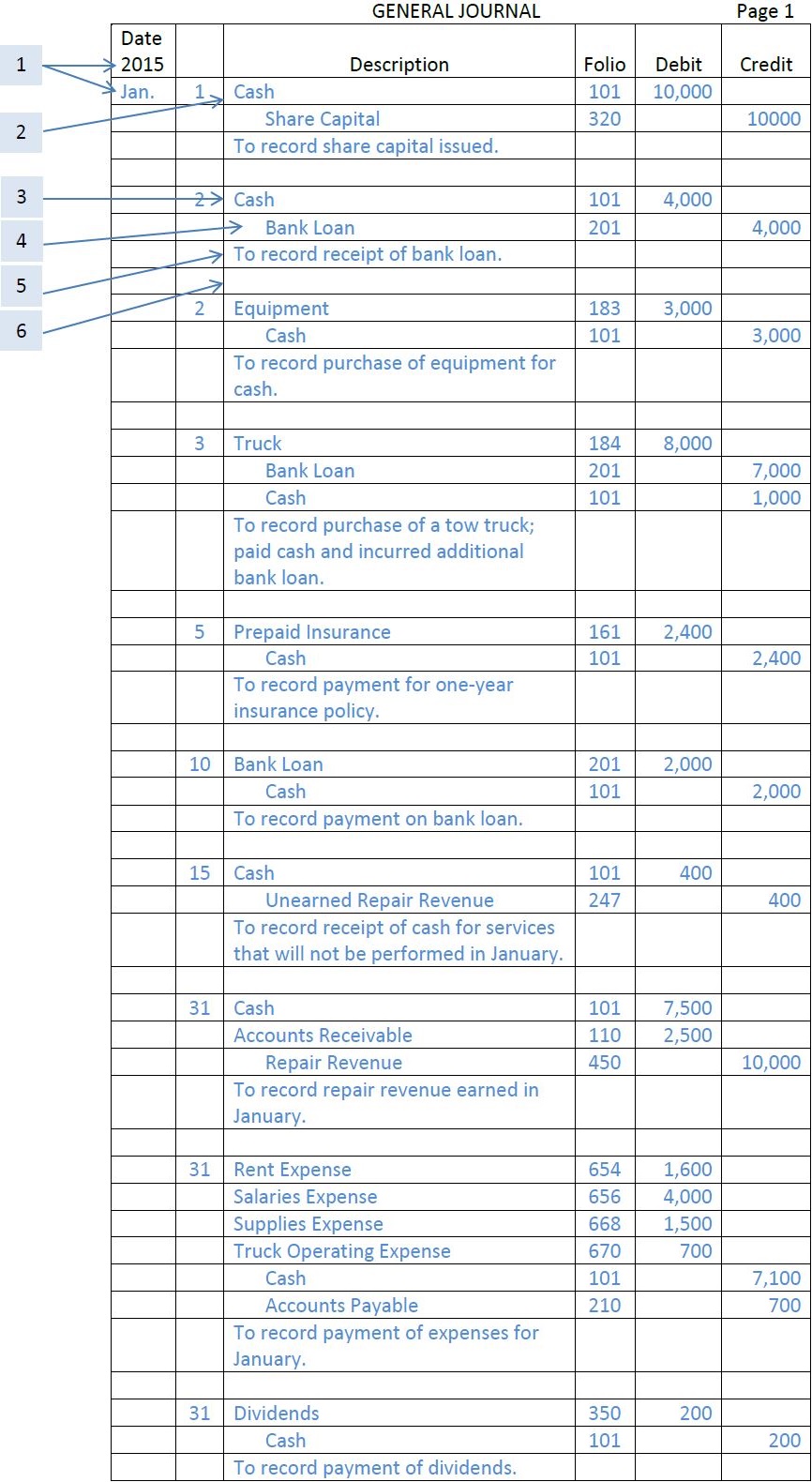

Each transaction is first recorded in the journal. The January transactions of Big Dog Carworks Corp. are recorded in its journal as shown in Figure 2.2. The journalizing procedure follows these steps (refer to Figure 2.2 for corresponding numbers):

- The year is recorded at the top and the month is entered on the first line of page 1. This information is repeated only on each new journal page used to record transactions.

- The date of the first transaction is entered in the second column, on the first line. The day of each transaction is always recorded in this second column.

- The name of the account to be debited is entered in the description column on the first line. By convention, accounts to be debited are usually recorded before accounts to be credited. The column titled Folio indicates the number given to the account in the General Ledger. For example, the account number for Cash is 101. The amount of the debit is recorded in the debit column.

- The name of the account to be credited is on the second line of the description column and is indented about one centimetre into the column. Accounts to be credited are always indented in this way in the journal. The amount of the credit is recorded in the credit column.

- An explanation of the transaction is entered in the description column on the next line. It is not indented.

- A line is usually skipped after each journal entry to separate individual journal entries and the date of the next entry recorded. It is unnecessary to repeat the month if it is unchanged from that recorded at the top of the page.

Figure 2.2 January General Journal Transactions for BDCC

Most of Big Dog’s entries have one debit and credit. An entry can also have more than one debit or credit, in which case it is referred to as a compound entry. The entry dated January 3 is an example of a compound entry.

- 31705 reads