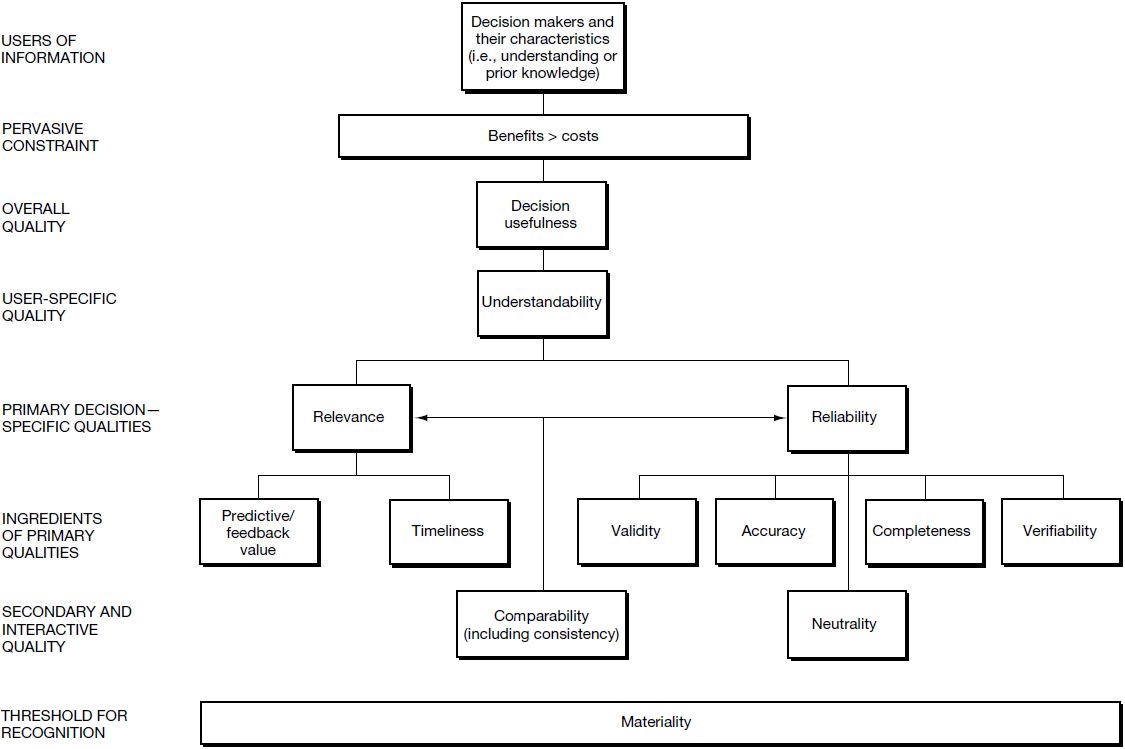

To provide output useful for assisting managers and other users of information, an IS must collect data and convert them into information that possesses important qualities. Table 1.1 describes qualities of information that, if attained, will help an organization achieve its business objectives. Figure 1.6 presents an overview of information qualities depicted as a hierarchy.

You can see that effectiveness overlaps with other qualities as it includes such measures as “timely” (i.e., availability) and “correct” (i.e., integrity). The effectiveness of information must be evaluated in relation to the purpose to be served—decision making. Effectiveness, then, is a function of the decisions to be made, the method of decision making to be used, the information already possessed by the decision maker, and the decision maker’s capacity to process information. The higher level factors in Figure 1.6, such as “users of information” and “overall quality (decision usefulness),” provide additional emphasis for these points. 1

|

Review Question Refer to Figure 1.5. Characterize the horizontal information flows and the vertical information flows. |

|

Effectiveness: deals with information being relevant and pertinent to the business process as well as being delivered in a timely, correct, consistent, and usable manner. Efficiency: concerns the provision of information through the optimal (most productive and economical) usage of resources. Confidentiality: concerns the protection of sensitive information from unauthorized disclosure. Integrity: relates to the accuracy and completeness of information as well as to its validity in accordance with business values and expectations. Availability: relates to information being available when required by the business process now and in the future. It also concerns the safeguarding of necessary resources and associated capabilities. Compliance: deals with complying with those laws, regulations, and contractual obligations to which the business process is subject, i.e., externally imposed business criteria. Reliability of Information: relates to the provision of appropriate information for management to operate the entity and for management to exercise its financial and compliance reporting responsibilities. Source: Reprinted with permission from COBIT: Control Objectives for Information and Related Technology—Framework, 3rd ed. (Rolling Meadows, IL: The Information Systems Audit and Control Foundation, 2000): 14. |

Understandability enables users to perceive the information’s significance. For example, information must be in a language understood by the decision maker. By language, we mean native language, such as English or French, as well as technical language, such as one that might be used in physics or computer science. Information that makes excessive use of codes and acronyms may not be understandable by some decision makers.

Information capable of making a difference in a decision-making situation by reducing uncertainty or increasing knowledge has relevance. For example, a credit manager making a decision about whether to grant credit to a customer might use the customer’s financial statements and credit history because that information could be relevant to the credit-granting decision. The customer’s organization chart would not be relevant. The description of reliability of information in Table 1.1 uses the term “appropriate.” Relevance is a primary component of appropriateness.

Information that is available to a decision maker before it loses its capacity to influence a decision has timeliness. Lack of timeliness can make information irrelevant. For example, the credit manager must receive the customer’s credit history before making the credit-granting decision. Otherwise, if the decision must be made without the information, the credit history becomes irrelevant. Table 1.1 describes availability as “being available when required.” Thus, availability can increase timeliness.

Predictive value and feedback value improve a decision maker’s capacity to predict, confirm, or correct earlier expectations. Information can have both types of value. A buyer for a retail store might use a sales forecast—a prediction—to establish inventory levels. As the buyer continues to use these sales forecasts and to review past inventory shortages and overages—feedback—he or she can refine decision making concerning inventory.

If there is a high degree of consensus about the information among independent measurers using the same measurement methods, the information has verifiability. Real estate assets are recorded in financial records at their purchase price. Why? Because the evidence of the assets’ cost provides an objective valuation for the property at that point.

Neutrality or freedom from bias means that the information is reliably represented. For example, the number of current members of a professional association may be overstated due to member deaths, career changers who don’t bother to quit, or members listed twice because of misspellings or address changes. Notice that verifiability addresses the reliability of the measurement method (e.g., purchase price vs. current value) and neutrality addresses the reliability of the entity doing the measuring.

Comparability is the quality that enables users to identify similarities and differences in two pieces of information. If we can compare information about two similar objects or events, the information is comparable. Comparing vendor pricing estimates where one vendor gives a per unit price, and another a price per case is problematic in choosing a low-cost vendor.

If, on the other hand, we can compare information about the same object or event collected at two points in time, the information is consistent. Analyzing sales growth, for example, might require horizontal or trend analysis for two or more years for one company.

As noted in Table 1.1, integrity is an information quality that can be expanded into three very important qualities: validity, accuracy, and completeness. In Figure 1.6 these are components of reliability. Information about actual events and actual objects has validity. For example, suppose that the IS records a sale and an account receivable for a shipment that didn’t actually occur. The recorded information describes a fictitious event; therefore, the information lacks validity.

Accuracy is the correspondence or agreement between the information and the actual events or objects that the information represents. For example, if the quantity on hand indicated on an inventory report was 51 units, when the actual physical quantity on hand was 15 units whether the cause was a transposed number or an erroneous count, the information is inaccurate.

Completeness is the degree to which information includes data about every relevant object or event necessary to make a decision. We use relevant in the sense of all objects or events that we intended to include. For instance, suppose that a shipping department prepared 50 shipping notices for 50 actual shipments made for the day. Two of the notices fell to the floor and were discarded with the trash. As a result, the billing department prepared customer invoices for only 48 shipments, not for 50.

In summary, there are many ways to measure the effectiveness of information. Those discussed above and included in Table 1.1 and Figure 1.6 include: understandability,relevance (or reliability), timeliness (or availability), predictive value, feedback value, verifiability,neutrality (or freedom from bias), comparability, consistency, integrity (or validity,accuracy, and completeness). These qualities appear again, in addition to some not discussed here (efficiency, confidentiality, and compliance), in subsequent chapters.

|

Review Question What are the qualities of information presented in this chapter? Explain each quality in your own words and give an example of each. |

Costs and Benefits of Information

We often hear people say that, before an action is undertaken, the estimated benefits of that action should exceed the estimated costs. This is a basic expectation, as basic as the American assumption that truth, justice, and the American way will prevail. In business, we make an assumption that there is a cost associated with each improvement in the quality of information. For example, the information reflected in an inventory data store could be improved if it were checked against a physical count of inventory each week. But imagine how costly that would be! Many companies use perpetual inventory balances for most of the year, or estimate their inventory balances based on sales or past years’ levels.

In practice, the benefits and sometimes the costs of information are often hard to measure. Chapter 6 provides some ideas for measuring the costs and benefits of an information system.

Conflicts Among Information Qualities

It is virtually impossible to achieve a maximum level for all of the qualities of information simultaneously. In fact, for some qualities, an increased level of one requires a reduced level of another. As one instance, obtaining complete information for a decision may require delaying use of the information until all events related to the decision have taken place. That delay may sacrifice the timeliness of the information. For example, to determine all the merchandise shipments made in November, an organization may have to wait until several days into December to make sure that all shipments get recorded.

As another example, to obtain accurate information, we may carefully and methodically prepare the information, thus sacrificing its timeliness. To ensure the accuracy of a customer invoice, billing clerks might check the invoice for accuracy several times and then get their supervisor to initial the invoice, indicating that she also has checked the invoice for accuracy. Though ensuring accuracy, these procedures certainly hurt timeliness.

Prioritizing Information Qualities

In cases where there are conflicts between qualities of information, defining a hierarchy establishes the relative importance of each quality. We could decide that accuracy is more important than any other quality. Or we could insist that timeliness be achieved even if that means that accuracy is sacrificed. For example, a marketing manager wanting to know quickly the impact of a new advertising campaign might check sales in just a few regions to get an early indication. The information may be timely, but it might be collected so hastily that it has limited reliability.

In some situations, managers choose to sacrifice maximum attainment of individual goals or values for achievement of a higher goal. For many decision makers, relevance of information is the key quality when choosing among many viable options. Maximizing one objective, rather than obtaining the highest possible levels for individual subordinate values, is a strategic choice. Later chapters revisit these information qualities and their role in the design, control, and use of various business processes.

- 56462 reads