While many BR functions support a wide range of managers and decision makers in an organization, some financially oriented business-reporting activities remain in the purview of the finance function. Information Systems typically support ad hoc (i.e., on demand) business reporting for the benefit of all decision makers who access data through easy-to-use business intelligence software. Periodic (i.e., regularly scheduled) business reports, such as the financial reports produced by the financial function from the data stored in the general ledger, are also supported by the Information Systems function. In this section we focus on the role of the general ledger in the BR process and the interactions between the general ledger and its relevant environment.

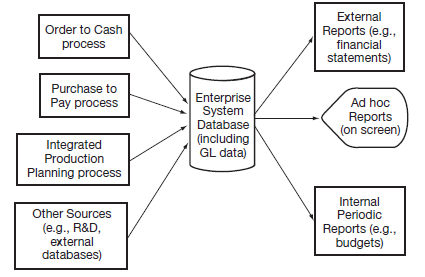

Before we begin, we should define a term that is used in this section and throughout the chapter. A feeder process is any business process that accumulates businessevent data that are then communicated to and processed within the enterprise system database (and to the general ledger within that database). Accordingly, the feeder processes include all those discussed in the earlier business process chapters, as shown in Figure 15.1. Business event data flow into the enterprise database, from which both periodic and ad hoc reports are produced. The general ledger comprises the accumulation of financially related business event data, providing summary-level data to the financial functions.

|

|

Consider how the information flows in Figure 15.1 are affected by integrated enterprise systems. The flows from feeder processes to the integrated database permit the consolidation of data, without creating separate physical copies of this data. For example, the general ledger data flows directly from the business processes along with nonfinancial business event data and does not have to be stored separately in its own file or database. The output side from the enterprise systems is much the same, providing information that can be extracted by the respective departments or managers using either pre-established reporting forms or queries of the enterprise system data. |

Because financial and nonfinancial data are truly integrated, analysts can focus on the provision of more complex and interesting information that can be used to increase the effectiveness and efficiency of the organization’s operations and strategies. We will explore some of the possibilities within this extended business reporting capability later in this chapter.

|

|

As we look to emerging capabilities, we should also consider how the external reporting model is changing. Increasingly, organizations are deciding to make financial information available on the Internet. Currently, there is little standardization to this information between companies. Figure 15.2 provides a diagram that synthesizes these various financial information flows in what is labeled the “financial information chain.” Note that the “operational data stores” are the central enterprise system database or other business reporting system data storage. From this data store(s), information is extracted for internal reporting (i.e., the reports on the left hand side of the diagram). Note that for external reporting, however, the information must be first filtered through the chart of accounts and the general ledger. Additional formatting may be required for special-purpose reports, such as those submitted to the Securities and Exchange Comission (SEC) or publication of the statements on the Web. Later in this chapter, we will discuss current efforts to improve the standardization and quality of this information to improve the efficiency and effectiveness of business reporting. |

- 4362 reads