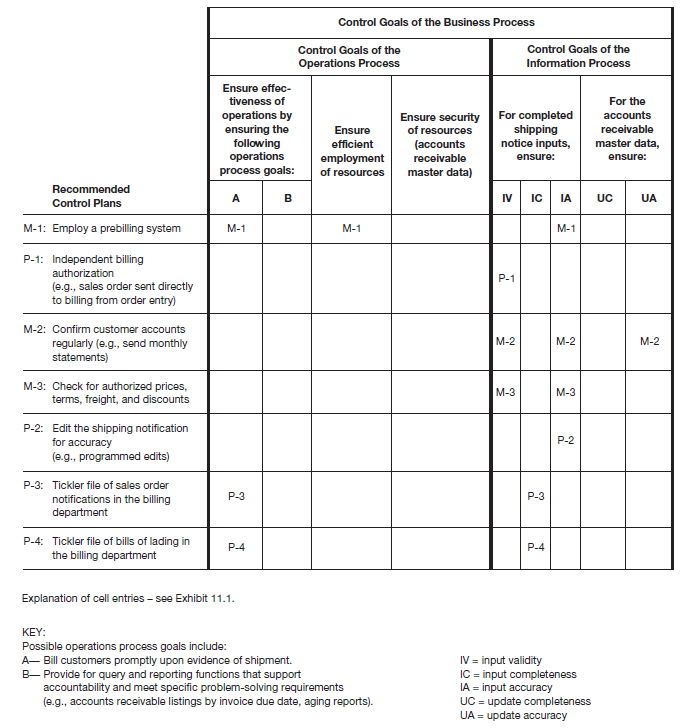

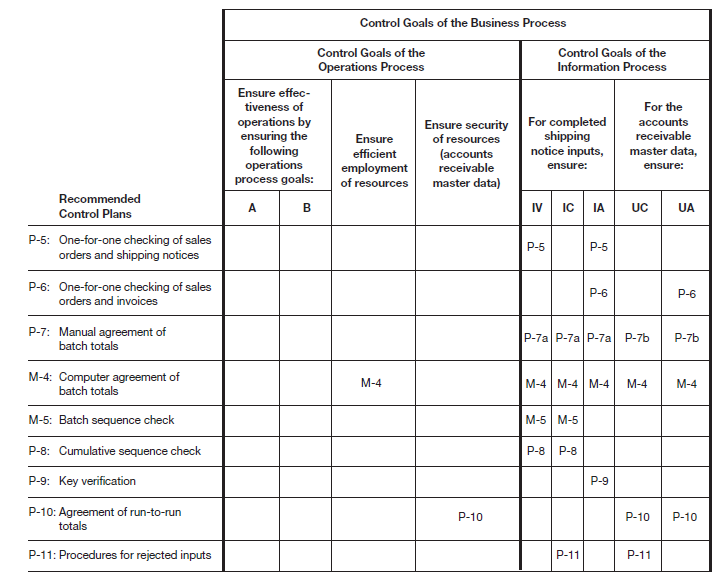

Each of the recommended control plans listed in the first column of the control matrix is discussed in Table 12.2. This exhibit is divided into two sections:

- A. Billing process control plans that are unique to the billing process.

- B. Controls for the processing technology in place or that apply to any business process. Your study of CONTROLLING INFORMATION SYSTEMS: PROCESS CONTROLS supplies understanding of how these plans relate to specific control goals. In other words, you should be able to explain the cell entries in Figure 12.8 for these four control plans. If you cannot do so readily, review CONTROLLING INFORMATION SYSTEMS: PROCESS CONTROLS.

|

Review Question What controls are associated with the billing function? Explain each control. |

As usual, you will find that some of the recommended control plans are present in the process and others are missing. As you study the control plans, be sure to notice where they are located on the systems flowchart.

|

A. Billing Process Control Plans M-1: Employ a prebilling system. Operations process goal A: If a prebilling system were used, it would shorten the time needed to bill customers and thus help to ensure operations process goal A—to bill customers promptly upon evidence of shipment. Upon notification that the shipment has been made, billing the customer involves simply releasing (mailing) the customer copy of the invoice. Efficient employment of resources: By collapsing two processes—preparing the sales order and generating the customer invoice—into a single operation, a prebilling system employs system resources more efficiently. Completed shipping notice input accuracy: Collapsing sales order preparation and customer invoice generation into a single operation improves billing accuracy by eliminating a separate data entry step. P-1: Independent billing authorization. Completed shipping notice input validity: Comparison of sales orders, received directly from order entry, with shipping notifications received from shipping, reduces the possibility that shipping notifications are invalid by verifying that each shipment is supported by an approved sales order. M-2: Confirm customer accounts regularly. Completed shipping notice input validity, Completed shipping notice input accuracy: The customer can be a means of controlling the billing process. By sending regular customer statements, we use the customer to check that invoices were valid and accurate. Most organizations send statements, but that process is beyond the scope depicted in Figure 12.6. Accounts receivable master data update accuracy: Because statements are produced from the accounts receivable master data, the customer also determines the accuracy of accounts receivable updates. M-3: Check for authorized prices, terms, freight, and discounts. Completed shipping notice input validity: The billing process in Figure 12.6 seems to have no explicit, independent check for authorized prices, terms, discounts, and freight charges. Note that the word “authorized” speaks to the control goal of input validity. The system should access a file containing approved pricing, which may be stored at the product or customer level. Completed shipping notice input accuracy: Having prices, terms, discounts, and freight charges independently checked by a second person helps to ensure input accuracy. Because much of the information necessary to calculate these amounts is not known until after shipment, we would expect to see prices, terms, freight, and discounts being calculated during the billing process by using an approved set of criteria. At a minimum, we would expect to see access to the inventory master data for a price check for the items shipped. Criteria for the terms, discount, and freight might be located on the customer master data (or accounts receivable master data) or within the billing program. P-2: Edit the shipping notification for accuracy. Completed shipping notice input accuracy: The output of the “Error and summary report” in Figure 12.6 implies that the update run performs some programmed edits. Programmed edits greatly increase the accuracy of entering sales data by using the computer to edit the data input. P-3 and P-4: Tickler files. Bill customers promptly, Completed shipping notice input completeness: Figure 12.6 includes two instances of this control plan. Monitoring the first tickler file (P-3) ensures that all shipping notices are received from shipping in a timely manner. Monitoring the second file (P-4) ensures that allinvoices are prepared in a timely manner. P-5 and P-6: One-for-one checking of outputs to inputs. Completed shipping notice input accuracy: One-for-one checking occurs in Figure 12.6 as follows:

Each of these instances of one-for-one checking helps ensure that data entered are accurate. Matching the shipping notification with the sales order, for example, checks that the quantity ordered is the quantity shipped. Completed shipping notice input validity: In the case of plan P-5, the goal of shipping notice input validity is addressed because no shipping notice is processed unless it is supported by an authorizedsales order. Completed shipping notice update accuracy: Matching the invoice—an output of the update process—with the sales order (P-6) verifies that the updates are accurate. B. Technology-Related Control Plans P-7: Manual agreement of batch totals. Completed shipping notice input validity, completeness, and accuracy: The broken line from that batch total to the key-to-disk computer screen display at the bottom of the data preparation column (annotated P-7a) indicates a reconciliation of the input totals to the totals of the inputs actually recorded in the sales event data. If we assume that the batch total is either a dollar total or hash total, we are justified in making cell entries in all three columns: input validity (IV), input completeness (IC), and input accuracy (IA). On the other hand, item or line counts help to ensure IC and IA (not IV), while document or record counts address the goal of IC only. Accounts receivable master data update completeness and accuracy: Another instance of manually verifying batch totals is depicted by the broken line (annotated P-7b) that connects the batch total file at the bottom of the data preparation column with the “Error and summary report” appearing in the computer operations column. Note that in this case, input totals are being reconciled to output totals (i.e., those resulting from updating the accounts receivable master data). Therefore, we show entries in the columns for update completeness (UC) and update accuracy (UA). Again, if the batch totals comprised only document/record counts, we could not justify a cell entry in the UA column. M-4: Computer agreement of batch totals. Efficient employment of resources: Computer agreement of batch controls improves efficiency through automation of the process. Input and update control goals: This control does not appear in the flowchart nor is it mentioned in the physical process description narrative. Therefore we cannot make any of the P (present) entries made for control plan P-7. M-5: Batch sequence check. Completed shipping notice input validity and completeness: To apply this control, the data entry clerk first must enter the range of serially numbered documents that comprise each batch. There is no evidence that this is being done in Figure 12.6, so we cannot determine if extra shipping notices are input (IV) or if any valid notices are not input (IC). P-8: Cumulative sequence check. Completed shipping notice input completeness: A cumulative sequence check matches the serial numbers of individual inputs—in this case shipping notices—against data containing all possible serial numbers—in this case all sales order numbers. In Figure 12.6, the “Cumulative numerical sequence” (of sales order numbers) stored on the disk in computer operations controls the input of the shipping notices. Either a batch sequence check or a cumulative sequence check—by accounting for allof the numbers preprinted on input documents—helps to ensure input completeness (IC). Completed shipping notice input validity: Because duplicate numbers are rejected, input validity is assured because an actual shipment of goods cannot be recorded twice (i.e., the second instance of the same document number must be invalid). P-9: Key verification. Completed shipping notice input accuracy: A second data entry clerk rekeying the data elements comprising each input record ensures the input accuracy (IA) of the keying done by the first clerk. P-10: Agreement of run-to-run totals. Security of resources, Update completeness, Update accuracy: If we assume that the “Error and Summary Report” includes a total of the accounts receivable master data before and after update (e.g., dollar totals of outstanding invoices) and the total dollars of new invoices, then the agreement process depicted by the dotted line at P-10 on Figure 12.6 ensures the integrity of the master data update. P-11: Procedures for rejected inputs. Input and update completeness: In Figure 12.6, rejected items are logged in two ways: They are printed on the “Error and summary report,” and they are also written to the “Error suspense data” that contain all rejected items not yet corrected. The cell entries in the IC and UC columns of the control matrix presume that corrective action will be taken to investigate all rejected items, remedy any errors, and resubmit the corrected input for reprocessing. We can include UC because the report is produced after the update. Note: In the control matrix of Figure 12.8, we do not include the operations process goal, “To comply with the fair pricing requirements of the Robinson-Patman Act,” because we believe that this goal relates more to the M/S process than to RC. However, were this goal column included in the billing function control matrix, plan M-3 would appear as a cell entry in that column. The independent check of authorized billing prices, terms, and the like helps to ensure that the company does not engage in discriminatory pricing practices in violation of the Robinson-Patman Act. |

- 6886 reads