Available under Creative Commons-ShareAlike 4.0 International License.

Managerial advice offered by headquarters, headquarters overhead, royalties on patents and trademarks, international computer hookups, ongoing costs of corporate R&D facilities, and other services rendered by the parent company or by one subsidiary to another are very difficult to price. For this reason they can be suitable conduits for moving funds from one place to another.

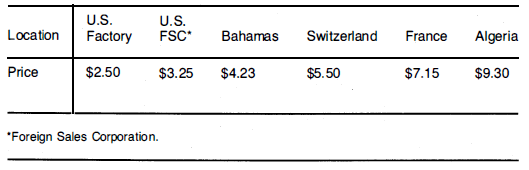

Figure 12.7 Chain Invoicing: Adding a 30% Commission at Each Stage

Fees for licensing and other contractual arrangements, as well as payments for services, can take any one of the following forms:

- A specific price per unit of product and/or pound of output

- A specific percentage of sales price

- A fixed sum per year (perhaps combined with one of the above two fees )

Rutenberg recommends that a financial manager take the following steps: 1

- Prepare a list of every conceivable fee, royalty, or service charge.

- Eliminate those that are not tax-deductible in either of the countries involved.

- Calculate the tax costs (income + withholding tax) and list the flows in descending order by total tax cost.

- List the flows again in terms of the probability that their omission would be noticed by the officials in either country.

- 2471 reads