As explained in the introduction to this chapter, North Americans have been used to treating the economy as a closed system. Traditionally the economy was considered to encompass only the goods and services produced by the people in a given country, which are then consumed by the same people. No interaction with the rest of the world was incorporated into the model; it was assumed that the people of the country, under the direction of the country's government, produce and consume whatever they need.

Today's economies, however, are not closed to external interactions. A rather substantial portion of the products and services produced in a country find their way to some other country. By the same token, a fairly large portion of the goods and services consumed by a country come from places several thousands of miles away.

To account for new sources of production and consumption—the international market—our model of the closed economy must be expanded on both sides of the equilibrium equation. In other words, our equilibrium condition

Y = C + I + G

(output equals expenditures) must be changed so as to reflect the added source of output as well as the added source of consumers.

Closed Economy: Total Available Output = GNP = Y

Total

Expenditures = C + I + G

Open Economy: Total Available Output = GNP = Y + Imports (M)

Total

Expenditures = C + I + G + Exports (X)

In other words, imports (M) represent additions to the domestic output (payments) which increase the total available output. Exports (X), on the other hand, represent increases in the total expenditures (incomes). Thus, the final position of the GNP in an open economy will depend on the net effect of the transactions—that is, the difference between imports and exports.

The net effect of international transactions on domestic GNP can be represented as imports minus exports (M - X), or N. Thus, the GNP in an open economy is represented by the sum C + I + G + N.

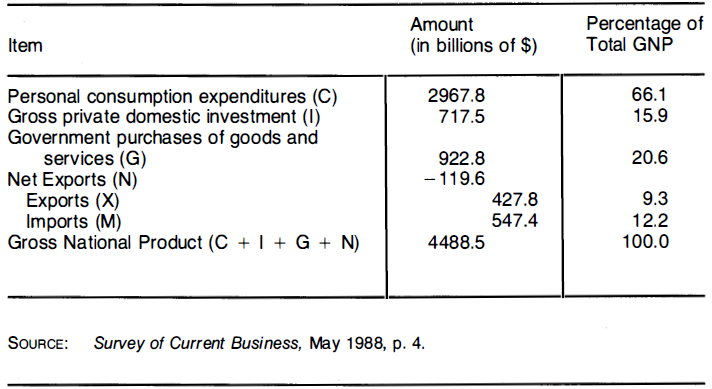

Figure 6.3 shows the U.S. GNP for 1987. As the table shows, the end result of the international transactions of the United States for that year was negative (a deficit): -$119.6 billion. As a result of this deficit, the GNP was $4488.5 billion.

- 2760 reads