Economists think of an economy as a productive system that converts natural and human resources into products that are traded in an open market and are eventually consumed. Thus, the basic model of an economy consists of a production subsystem and a consumption subsystem. These two subsystems are at equilibrium when whatever is produced is actually consumed.

The basic concept used by economists to describe the production subsystem of an economy is the gross national product, or GNP. 1 The GNP is the sum of the money values of all final goods and services produced during a specific period of time, usually a year. The concept economists use to describe the consumption subsystem is aggregate demand. Aggregate demand is the total amount of money that all consumers, business firms, and government agencies wish to spend on all final goods and services. This aggregate demand disaggregates, so to speak, into its three constituent parts:

- Consumer expenditures (consumption), designated by C

- Investment spending (the sum of expenditures by business firms in new plants and equipment plus the expenditures of households on new homes), designated by I

- Government purchases of goods and services, designated by G

A third main concept is national income. National income is the total income received by the citizens of a country for the services they perform. When taxes are excluded from national income, what remains is disposable income.

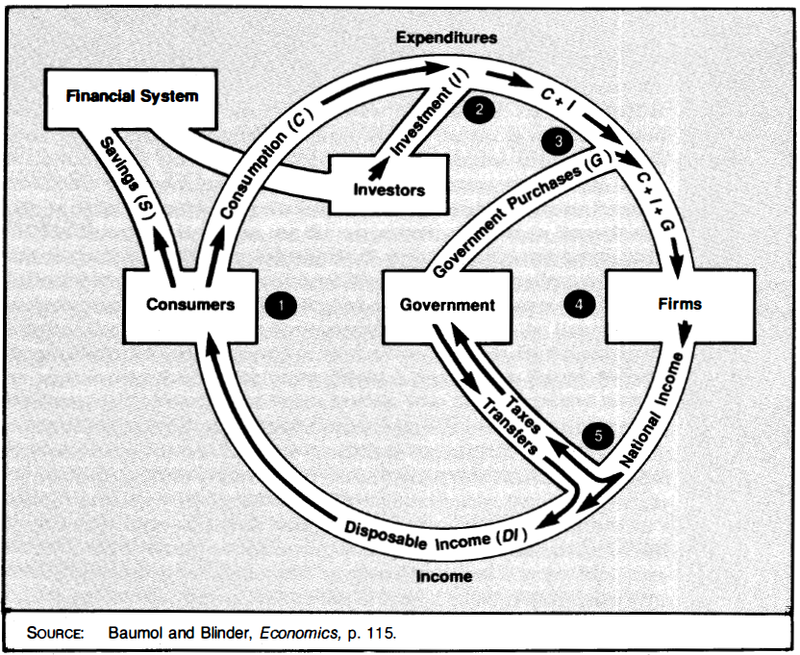

The interactions and relationships among these concepts are graphically represented in the circular flow diagram in Figure 6.1, which depicts the economic system as a set of tubes into which fluids are injected or from which they leak out. The three boxes in the center of the diagram represent the three main actors in the system—consumers, government, and business. The other two boxes represent the financial system, which accepts funds from consumers and pumps them into the aggregate demand, and investors, who channel the funds into the system to the firms that produce the gross national product.

The upper half of this circular flow diagram depicts the flow of expenditures on goods and services, which comes from consumers (point 1), investors (point 2), and government (point 3) and goes to the firms that produce the output (point 4). The lower half of the diagram indicates how the income paid out by firms (point 4) flows to consumers (point 1), after some is siphoned off by the government in the form of taxes and part is replaced by transfer payments (point 5).

Ideally the system depicted in the diagram will be in equilibrium. That is to say, the production (supply) side will equal the consumption (demand) side:

Y = C + I + G

This equation states the first law of economics:

National product and national income must be equal.

Although there are no notable differences among definitions of the concept of GNP, there are quite a few differences in the ways nations measure this economic parameter. As a rule, however, most nations employ one of the following methods of measuring GNP.

- 2130 reads