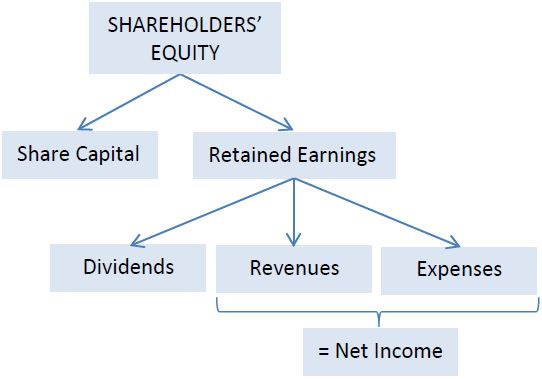

Chapter 1 explained that shareholders’ equity represents the net assets owned by the owners of a corporation. There are five different types of shareholders’ equity accounts: share capital, retained earnings, dividends, revenues, and expenses. Share capital represents the investments made by owners into the business and causes shareholders’ equity to increase. Retained earnings is the sum of all net incomes earned over the life of the corporation to date, less any dividends distributed to shareholders over the same time period.

Therefore, the Retained Earnings account includes revenues, which cause shareholders’ equity to increase, along with expenses and dividends, which cause shareholders’ equity to decrease. Figure 2.1 summarizes shareholders’ equity accounts.

- 3416 reads