Available under Creative Commons-NonCommercial-ShareAlike 4.0 International License.

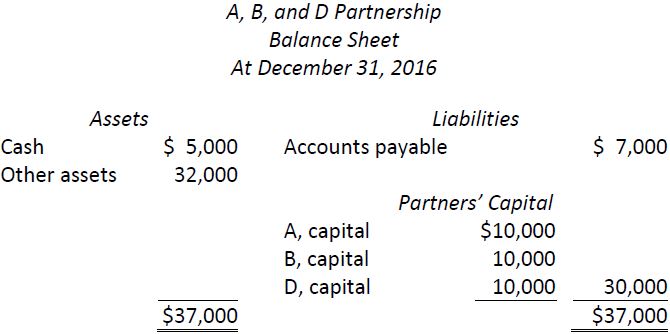

This method is similar to the purchase of an existing partner’s interest. Assume C sells a partnership interest to D. Payment for the ownership interest is a private transaction, though the existing partners must approve the new arrangement. There is no change in either the assets or the capital of the partnership as a result of this transaction. However, the following journal entry would be made:

The balance sheet would show the following:

- 2584 reads