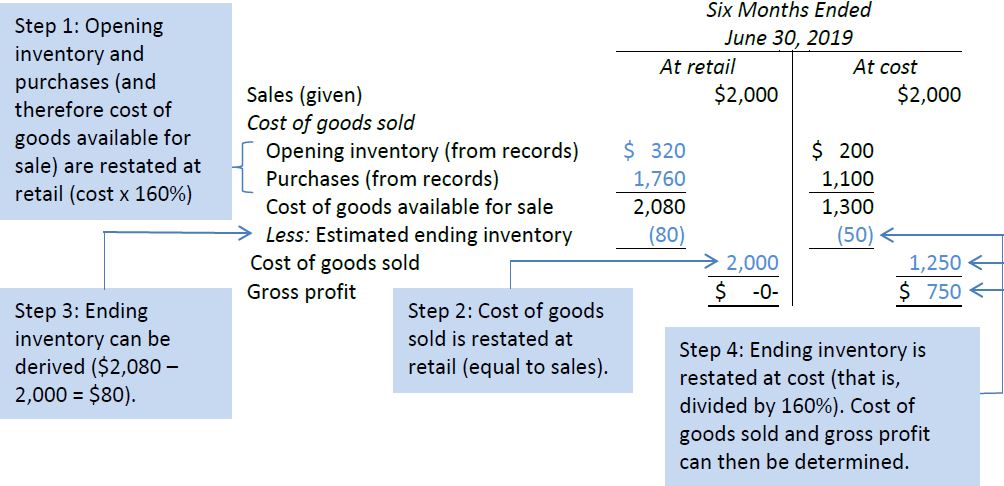

The retail inventory method is another means to estimate cost of goods sold and ending inventory. It can be used when items are consistently valued at a known percentage of cost, known as a markup. A mark-up is the ratio of retail value (or selling price) to cost. For example, if an inventory item had a cost of $10 and a retail value of $12, it was marked up to 120% (12/10 x 100). Mark-ups are commonly used in clothing stores.

First, the cost of goods available for sale is converted to its retail value (the selling price). To do this, the mark-up must be known. Assume the same information as above for Pete’s Products Ltd., except that now every item in the store is marked up to 160% of its purchase price. That is, if an item is purchased for $100, it is sold for $160. Based on this, opening inventory, purchases, and cost of goods available can be restated at retail. Cost of goods sold can then be valued at retail, meaning that it will equal sales for the period. From this, ending inventory (at retail) can be determined, then converted back to cost using the mark-up. These steps are illustrated below.

The retail inventory method of estimating ending inventory is easy to calculate and produces a relatively accurate cost of ending inventory, provided that no change in the average mark-up has occurred during the period.

- 2953 reads