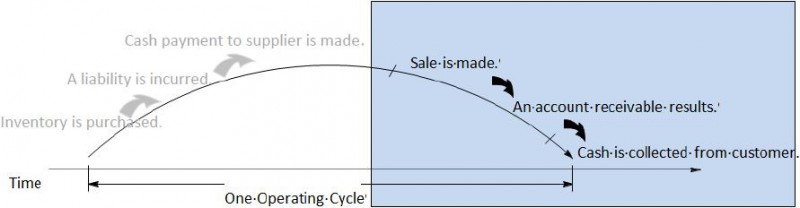

As discussed in an earlier chapter, the sale of inventory and resulting collection of receivables are part of a business’s operating cycle as shown in Figure 13.3.

A business’s revenue operating cycle is a subset of the operating cycle and includes the purchase of inventory, the sale of inventory and creation of an account receivable, and the generation of cash when the receivable is collected. The length of time it takes BDCC to complete one revenue operating cycle is an important measure of liquidity and can be calculated by adding the number of days of sales in inventory plus the number of days it takes to collect receivables. The BDCC financial data required for this calculation follows.

In 2021, 153 days were required to complete the revenue cycle, compared to 117 days in 2020. So, if accounts payable terms require payment within 60 days, BDCC may not be able to pay them because the number of days to complete the revenue cycle for both 2020 (117 days) and 2021 (153 days) are significantly greater than 60 days.

- 2627 reads