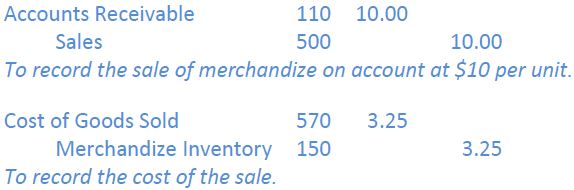

In Chapter 5 the journal entries to record the sale of merchandize were introduced. Chapter 5 showed how the dollar value included in these journal entries is determined. We now know that the information in the inventory record is used to prepare the journal entries in the general journal. For example, the credit sale on June 23 using weighted average costing would be recorded as follows (refer to Figure 6.9).

Perpetual inventory incorporates an internal control feature that is lost under the periodic inventory system. Losses resulting from theft and error can easily be determined when the actual quantity of goods on hand is counted and compared with the quantities shown in the inventory records as being on hand. It may seem that this advantage is offset by the time and expense required to continuously update inventory records, particularly where there are thousands of different items of various sizes on hand. However, computerization makes this record keeping easier and less expensive because the inventory accounting system can be tied in to the sales system so that inventory is updated whenever a sale is recorded.

- 2841 reads