| LO1 – Explain how adjusting entries match revenues and expenses to the appropriate time period. |

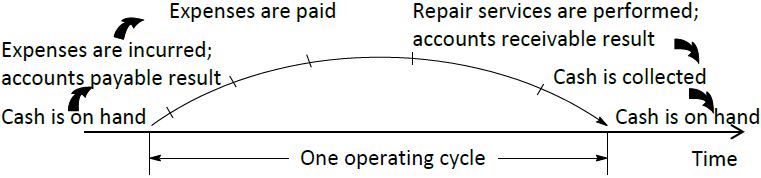

Financial transactions occur continuously during an accounting period as part of a sequence of operating activities. For Big Dog Carworks Corp., this sequence of operating activities takes the following form:

|

This cash-to-cash sequence of transactions is commonly referred to as the operating cycle and is illustrated in Figure 3.1.

Depending on the type of business, an operating cycle can vary in duration from short, such as one week (for example, a small grocery store) to much longer, such as one year (for example, a large construction company). Therefore, an annual accounting period could involve multiple operating cycles as shown in Figure 3.2.

Notice that not all of the operating cycles in Figure 3.2 are completed within the accounting period. Since financial statements are prepared at specific time intervals to meet the GAAP requirement of timeliness, it is necessary to consider how to record and report transactions related to the accounting period’s incomplete operating cycles. There are two criteria. These are discussed in the following section.

- 3359 reads