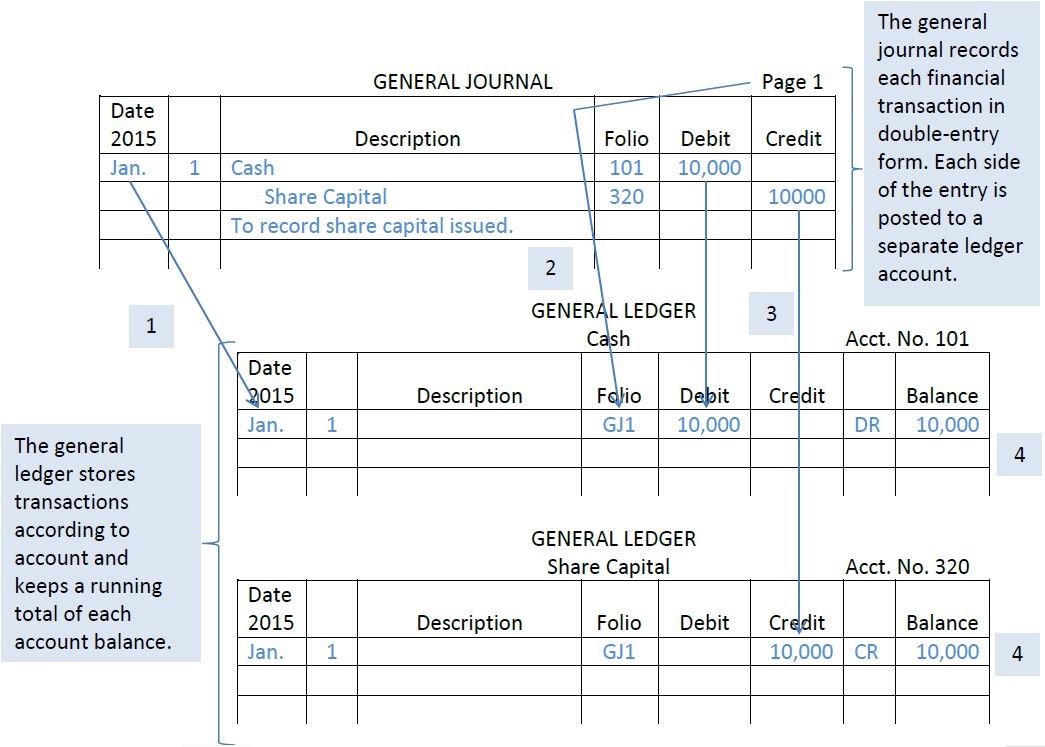

The ledger account is a formal variation of the T-account. The ledger accounts shown in Figure 2.3 are similar to what is used in electronic/digital accounting programs. Ledger accounts are kept in the general ledger. Debits and credits recorded in the journal are transferred or “posted” to appropriate ledger accounts so that the details and balance for each account can be found easily. Figure 2.3 uses the first transaction of Big Dog Carworks Corp. to illustrate how to post amounts and record other information. The posting procedure follows these steps (refer to Figure 2.3 for corresponding numbers):

- The date is recorded in the appropriate general ledger account.

- The general journal page number is recorded in the Folio column of each ledger account as a cross reference. In this case, the posting has been made from general journal page 1 so the reference is recorded as “GJ1”.

- The debit and credit amounts from the general journal are posted to the debit or credit columns in the appropriate general ledger account. Here the entry debiting Cash is posted to the Cash ledger account. The entry crediting share capital is then posted to the Share Capital general ledger account.

- After posting the entry, a balance is calculated in the Balance column of each general ledger account. A notation is recorded in the column to the left of the Balance column indicating whether the balance is a debit (DR) or credit (CR). A brief description can be entered in the Description column of the account but this is usually not necessary since the journal includes a detailed description for each journal entry.

This manual process of recording, posting, summarizing, and preparing financial statements is cumbersome and time-consuming. In virtually all businesses, the use of accounting software automates much of the process. In this and subsequent chapters, either the T-account or the general ledger account format will be used to explain and illustrate concepts.

- 12159 reads